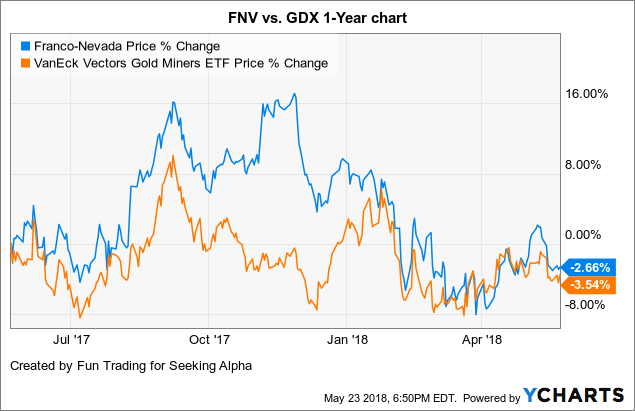

When writing about Manitex (MNTX), a small American manufacturer of boom truck cranes, knuckle-boom cranes, and other lifting equipment, I��ve often mentioned Tadano (6395.T) (OTC:TDNOF) as a peer/comparable, although Tadano and Manitex have relatively little direct overlap (some in rough terrain cranes and truck-mounted cranes). Now, these two companies will be even more closely tied together, as they announced a tie-up on Friday, May 25, that will see Tadano take a nearly 15% equity stake in the company.

Although the terms of the deal suggest to me that it��s slightly dilutive in the near term, Tadano��s investment should allow Manitex to retire a meaningful portion of its debt (perhaps around a third), reducing its operating risk and saving some interest expense, as well as help the company operationally. It could also, perhaps, be prelude to an eventual acquisition by Tadano. Although Manitex shares are no longer exceptionally cheap, there is still some upside here, particularly if Manitex can make faster progress growing its PM Group knuckle-boom crane business.

The DealThe two companies announced that Tadano will acquire 2.92 million shares of Manitex at a trailing average price of $11.19, or about $32 million. The deal should close at month��s end, and when it does, Tadano will own just under 15% of Manitex shares. Tadano will also be allowed to appoint one member to Manitex��s board, and the initial pick is Tadano��s CEO for the American operations, Ingo Schiller.

Introducing TadanoAs a relatively small company, overall ($1.5 billion in enterprise value and $1.6 billion in trailing sales), Tadano is not really a household name to most American investors. Likewise, although Tadano technically has an ADR ticker, I believe it is essentially a placeholder ticker with no volume.

Although small, I believe Tadano can punch above its weight. Along with Kato Works, Tadano basically controls the Japanese market for rough terrain cranes with approximately 45% to 50% share (Kato holding around 40% to 45% share). Tadano also holds around 25% of the U.S. market for rough terrain cranes, 40%-plus of the Mideast market, 15% of the European market, and 40% of the ex-Japan Asian market. Tadano generates about 70% of its revenue from mobile cranes (rough terrain cranes, all-terrain cranes, and truck crane), another 10% to 15% from truck-loader cranes and truck-mounted aerial work platforms (each), and the remainder from parts, service, and used equipment. While Tadano has strong share in Japan with its truck-loader cranes and AWPs, those businesses aren��t so significant outside Japan today.

In Japan, rough terrain cranes are a favored choice for construction work, and virtually, all of Tadano��s Japanese sales are tied to construction in some form or fashion �� about a third from residential construction, a similar amount from non-residential construction, and 10% to 20% from infrastructure projects.

While rough terrain cranes hold more than 60% of the U.S. market for mobile cranes, Tadano hasn��t really penetrated markets like non-residential construction or infrastructure to a large extent. With that, about 70% of the company��s U.S. crane sales are tied to oil/gas applications. In Europe, Tadano��s efforts are limited by the fact that all-terrain cranes dominate the market, and while Tadano is building its all-terrain line-up, market leader Liebherr (with more than 50% share) benefits from a strong direct sales effort and the widest line-up of all-terrain cranes on the market.

Tadano��s primary competitors in the U.S. are Terex (TEX) and Manitowoc (MTW), both of which compete in rough terrain and all-terrain cranes. Tadano is not involved in tower cranes or crawler cranes, so Tadano��s overlap/impact on the overall sales of Terex and Manitowoc is somewhat limited. And, as I said before, Manitex and Tadano don��t compete head-to-head all that much �� there is some competition in rough terrain cranes, truck-mounted cranes, and specialized cranes, but really not that much.

Why Do This Deal?This is a potentially interesting deal for both Manitex and Tadano, though a lot rides on just how much of that potential can actually be realized in the coming years. For Manitex, arguably the biggest near-term benefit is gaining access to Tadano��s distribution network, and particularly for Manitex��s knuckle-boom cranes (PM Group). This remains a very high-potential opportunity for Manitex, but one that has been limited by the need to grow the distribution network to get more cranes in front of potential customers.

Tadano��s perspective on it is a little different and perhaps more interesting for the long term. Tadano��s management talked about looking for synergies in product development, sales, and in joint purchasing. If these two companies working together can reduce their supply chain costs in the North American market, that��s potentially a big deal �� every quarter-point of gross margin in my Manitex model is worth about $0.04 of EPS. Tadano may also stand to benefit from Manitex��s greater exposure to the U.S. construction markets �� while Manitex too was once much more dependent upon oil/gas-related demand, the company has successfully pivoted toward a more construction-driven business mix (though recovering energy markets are certainly helping the business now).

The OpportunityAlthough this deal appears slightly dilutive to Manitex in the near term (including lower interest expense and debt levels), improved procurement could potentially generate meaningful value from this deal, not to mention faster growth in the PM Group business. Although the shares look basically fairly valued on cash flow, I believe EBITDA-based valuation can support the shares into the mid-teens.

As for Tadano (for those investors who would consider investing in a Japanese stock), I think the shares offer double-digit long-term potential, but the near-term valuation is a little less compelling. Tadano recently reported another quarterly miss and reduced earnings expectations for the next fiscal year by more than 20% relative to prior sell-side expectations, though about half of that was tied to growth investments in the business. It��s also worth noting that the Japanese market, which generates around half of the company��s revenue, is likely going to see crane demand bottoming out from mid-2018 to mid-2019.

The Bottom LineTime will tell if this investment is a prelude to an acquisition of Manitex by Tadano. Japanese companies don��t often acquire American companies, but I can see how Manitex would offer some appealing product line extension opportunities and market expansion opportunities in North America and Europe (to a lesser extent). Even if Tadano��s ownership never goes beyond 15%, though, this is a respectable way for Manitex to raise funds to pare down debt while perhaps accelerating the business plan for PM Group and potentially attaining meaningful cost savings down the line.

Disclosure: I am/we are long MNTX.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

BitcoinX (CURRENCY:BCX) traded down 2.8% against the US dollar during the 1 day period ending at 23:00 PM ET on May 26th. BitcoinX has a market cap of $0.00 and $630,952.00 worth of BitcoinX was traded on exchanges in the last 24 hours. One BitcoinX coin can currently be bought for approximately $0.0178 or 0.00000244 BTC on exchanges including Gate.io, ZB.COM, Huobi and CoinEgg. During the last seven days, BitcoinX has traded 10.7% lower against the US dollar.

BitcoinX (CURRENCY:BCX) traded down 2.8% against the US dollar during the 1 day period ending at 23:00 PM ET on May 26th. BitcoinX has a market cap of $0.00 and $630,952.00 worth of BitcoinX was traded on exchanges in the last 24 hours. One BitcoinX coin can currently be bought for approximately $0.0178 or 0.00000244 BTC on exchanges including Gate.io, ZB.COM, Huobi and CoinEgg. During the last seven days, BitcoinX has traded 10.7% lower against the US dollar.

.jpg)